6. Multi-Risk Derivatives Portfolios¶

The step from multi-risk derivatives instruments to multi-risk derivatives instrument portfolios is not a too large one. This part of the tutorial shows how to model an economy with three risk factors

[1]:

from dx import *

from pylab import plt

plt.style.use('seaborn')

6.1. Risk Factors¶

This sub-section models the single risk factors. We start with definition of the risk-neutral discounting object.

[2]:

# constant short rate

r = constant_short_rate('r', 0.02)

Three risk factors ares modeled:

- geometric Brownian motion

- jump diffusion

- stochastic volatility process

[3]:

# market environments

me_gbm = market_environment('gbm', dt.datetime(2015, 1, 1))

me_jd = market_environment('jd', dt.datetime(2015, 1, 1))

me_sv = market_environment('sv', dt.datetime(2015, 1, 1))

Assumptions for the geometric_brownian_motion object.

[4]:

# geometric Brownian motion

me_gbm.add_constant('initial_value', 36.)

me_gbm.add_constant('volatility', 0.2)

me_gbm.add_constant('currency', 'EUR')

me_gbm.add_constant('model', 'gbm')

Assumptions for the jump_diffusion object.

[5]:

# jump diffusion

me_jd.add_constant('initial_value', 36.)

me_jd.add_constant('volatility', 0.2)

me_jd.add_constant('lambda', 0.5)

# probability for jump p.a.

me_jd.add_constant('mu', -0.75)

# expected jump size [%]

me_jd.add_constant('delta', 0.1)

# volatility of jump

me_jd.add_constant('currency', 'EUR')

me_jd.add_constant('model', 'jd')

Assumptions for the stochastic_volatility object.

[6]:

# stochastic volatility model

me_sv.add_constant('initial_value', 36.)

me_sv.add_constant('volatility', 0.2)

me_sv.add_constant('vol_vol', 0.1)

me_sv.add_constant('kappa', 2.5)

me_sv.add_constant('theta', 0.4)

me_sv.add_constant('rho', -0.5)

me_sv.add_constant('currency', 'EUR')

me_sv.add_constant('model', 'sv')

Finally, the unifying valuation assumption for the valuation environment.

[7]:

# valuation environment

val_env = market_environment('val_env', dt.datetime(2015, 1, 1))

val_env.add_constant('paths', 10000)

val_env.add_constant('frequency', 'W')

val_env.add_curve('discount_curve', r)

val_env.add_constant('starting_date', dt.datetime(2015, 1, 1))

val_env.add_constant('final_date', dt.datetime(2015, 12, 31))

These are added to the single market_environment objects of the risk factors.

[8]:

# add valuation environment to market environments

me_gbm.add_environment(val_env)

me_jd.add_environment(val_env)

me_sv.add_environment(val_env)

Finally, the market model with the risk factors and the correlations between them.

[9]:

risk_factors = {'gbm' : me_gbm, 'jd' : me_jd, 'sv' : me_sv}

correlations = [['gbm', 'jd', 0.66], ['jd', 'sv', -0.75]]

6.2. Derivatives¶

In this sub-section, we model the single derivatives instruments.

6.2.1. American Put Option¶

The first derivative instrument is an American put option.

[10]:

gbm = geometric_brownian_motion('gbm_obj', me_gbm)

[11]:

me_put = market_environment('put', dt.datetime(2015, 1, 1))

me_put.add_constant('maturity', dt.datetime(2015, 12, 31))

me_put.add_constant('strike', 40.)

me_put.add_constant('currency', 'EUR')

me_put.add_environment(val_env)

[12]:

am_put = valuation_mcs_american_single('am_put', mar_env=me_put, underlying=gbm,

payoff_func='np.maximum(strike - instrument_values, 0)')

[13]:

am_put.present_value(fixed_seed=True, bf=5)

[13]:

5.012

6.2.2. European Maximum Call on 2 Assets¶

The second derivative instrument is a European maximum call option on two risk factors.

[14]:

jd = jump_diffusion('jd_obj', me_jd)

[15]:

me_max_call = market_environment('put', dt.datetime(2015, 1, 1))

me_max_call.add_constant('maturity', dt.datetime(2015, 9, 15))

me_max_call.add_constant('currency', 'EUR')

me_max_call.add_environment(val_env)

[16]:

payoff_call = "np.maximum(np.maximum(maturity_value['gbm'], maturity_value['jd']) - 34., 0)"

[17]:

assets = {'gbm' : me_gbm, 'jd' : me_jd}

asset_corr = [correlations[0]]

[18]:

asset_corr

[18]:

[['gbm', 'jd', 0.66]]

[19]:

max_call = valuation_mcs_european_multi('max_call', me_max_call, assets, asset_corr,

payoff_func=payoff_call)

[20]:

max_call.present_value(fixed_seed=False)

[20]:

8.334

[21]:

max_call.delta('jd')

[21]:

0.7596

[22]:

max_call.delta('gbm')

[22]:

0.2824

6.2.3. American Minimum Put on 2 Assets¶

The third derivative instrument is an American minimum put on two risk factors.

[23]:

sv = stochastic_volatility('sv_obj', me_sv)

[24]:

me_min_put = market_environment('min_put', dt.datetime(2015, 1, 1))

me_min_put.add_constant('maturity', dt.datetime(2015, 6, 17))

me_min_put.add_constant('currency', 'EUR')

me_min_put.add_environment(val_env)

[25]:

payoff_put = "np.maximum(32. - np.minimum(instrument_values['jd'], instrument_values['sv']), 0)"

[26]:

assets = {'jd' : me_jd, 'sv' : me_sv}

asset_corr = [correlations[1]]

asset_corr

[26]:

[['jd', 'sv', -0.75]]

[27]:

min_put = valuation_mcs_american_multi(

'min_put', val_env=me_min_put, risk_factors=assets,

correlations=asset_corr, payoff_func=payoff_put)

[28]:

min_put.present_value(fixed_seed=True)

[28]:

4.296

[29]:

min_put.delta('jd')

[29]:

-0.0981

[30]:

min_put.delta('sv')

[30]:

-0.2102

6.3. Portfolio¶

To compose a derivatives portfolio, derivatives_position objects are needed.

[31]:

am_put_pos = derivatives_position(

name='am_put_pos',

quantity=2,

underlyings=['gbm'],

mar_env=me_put,

otype='American single',

payoff_func='np.maximum(instrument_values - 36., 0)')

[32]:

max_call_pos = derivatives_position(

'max_call_pos', 3, ['gbm', 'jd'],

me_max_call, 'European multi',

payoff_call)

[33]:

min_put_pos = derivatives_position(

'min_put_pos', 5, ['sv', 'jd'],

me_min_put, 'American multi',

payoff_put)

These objects are to be collected in dictionary objects.

[34]:

positions = {'am_put_pos' : am_put_pos, 'max_call_pos' : max_call_pos,

'min_put_pos' : min_put_pos}

All is together to instantiate the derivatives_portfolio class.

[35]:

port = derivatives_portfolio(name='portfolio',

positions=positions,

val_env=val_env,

risk_factors=risk_factors,

correlations=correlations)

Let us have a look at the major portfolio statistics.

[36]:

%time stats = port.get_statistics()

stats

Totals

pos_value 51.769

dtype: float64

CPU times: user 1.42 s, sys: 124 ms, total: 1.55 s

Wall time: 1.48 s

[36]:

| position | name | quantity | otype | risk_facts | value | currency | pos_value | pos_delta | pos_vega | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | am_put_pos | am_put_pos | 2 | American single | [gbm] | 3.182 | EUR | 6.364 | 1.2184 | 30.5422 |

| 1 | max_call_pos | max_call_pos | 3 | European multi | [gbm, jd] | 8.165 | EUR | 24.495 | {'gbm': 0.8646, 'jd': 2.2662} | {'gbm': 14.9805, 'jd': 10.35} |

| 2 | min_put_pos | min_put_pos | 5 | American multi | [sv, jd] | 4.182 | EUR | 20.910 | {'sv': -1.1675, 'jd': -0.6225} | {'sv': 8.322, 'jd': 11.352} |

[37]:

stats['pos_value'].sum()

[37]:

51.769000000000005

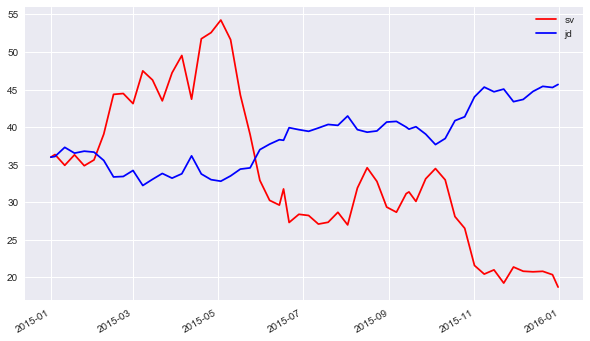

Finally, a graphical look at two selected, simulated paths of the stochastic volatility risk factor and the jump diffusion risk factor, respectively.

[38]:

path_no = 1

paths1 = port.underlying_objects['sv'].get_instrument_values()[:, path_no]

paths2 = port.underlying_objects['jd'].get_instrument_values()[:, path_no]

[39]:

paths1

[39]:

array([36. , 36.34884124, 34.9130166 , 36.31001777, 34.85894675,

35.63213975, 39.0707393 , 44.35899961, 44.47413556, 43.13168786,

47.48647475, 46.27393881, 43.49655379, 47.23009583, 49.53908109,

43.71731937, 51.76008829, 52.58524036, 54.2573447 , 51.6460015 ,

44.28088435, 39.01540236, 32.91109921, 30.24790867, 29.61667412,

31.76473582, 27.30258542, 28.39127869, 28.23333544, 27.08972766,

27.32993764, 28.65926992, 26.9785575 , 31.8938528 , 34.58971037,

32.7699367 , 29.35365969, 28.66856698, 31.14196767, 31.37051847,

30.10832392, 33.11928276, 34.48108709, 32.97416103, 28.08648082,

26.52705819, 21.57771857, 20.42912064, 20.99231801, 19.23163105,

21.37234395, 20.80944619, 20.73301676, 20.79953889, 20.34822548,

18.69820953])

[40]:

paths2

[40]:

array([36. , 36.09036184, 37.30618631, 36.53472814, 36.79572901,

36.66944957, 35.56227649, 33.3644349 , 33.42674479, 34.22659123,

32.22562864, 33.05209641, 33.82798732, 33.20431052, 33.78753542,

36.17164509, 33.76072474, 33.00278459, 32.79744011, 33.50195594,

34.40874205, 34.57037634, 37.00098086, 37.7309694 , 38.32223737,

38.2477447 , 39.92233666, 39.6591103 , 39.43998269, 39.88306801,

40.35338195, 40.23418088, 41.48106905, 39.66194269, 39.32622142,

39.48978055, 40.67396363, 40.76122376, 40.00499204, 39.725126 ,

40.05448393, 39.06546207, 37.674332 , 38.48264394, 40.86222422,

41.3749628 , 44.02458974, 45.32751049, 44.704871 , 45.06224883,

43.38741804, 43.68855748, 44.75023229, 45.4285521 , 45.27511078,

45.68070094])

The resulting plot illustrates the strong negative correlation.

[41]:

import matplotlib.pyplot as plt

%matplotlib inline

plt.figure(figsize=(10, 6))

plt.plot(port.time_grid, paths1, 'r', label='sv')

plt.plot(port.time_grid, paths2, 'b', label='jd')

plt.gcf().autofmt_xdate()

plt.legend(loc=0); plt.grid(True)

# negatively correlated underlyings

Copyright, License & Disclaimer

© Dr. Yves J. Hilpisch | The Python Quants GmbH

DX Analytics (the “dx library” or “dx package”) is licensed under the GNU Affero General Public License version 3 or later (see http://www.gnu.org/licenses/).

DX Analytics comes with no representations or warranties, to the extent permitted by applicable law.

http://tpq.io | dx@tpq.io | http://twitter.com/dyjh

Quant Platform | http://pqp.io

Python for Finance Training | http://training.tpq.io

Certificate in Computational Finance | http://compfinance.tpq.io

Derivatives Analytics with Python (Wiley Finance) | http://dawp.tpq.io

Python for Finance (2nd ed., O’Reilly) | http://py4fi.tpq.io